The Peruvian Tax Administration (SUNAT) published a resolution that establishes the procedure, deadlines and conditions for submitting the Ultimate Beneficiary Informative Return

Peru Tax Alert

Legislative Decree No. 1372, whose regulation was approved through Supreme Decree No. 003-2019-EF, established that legal persons and legal arrangements have the obligation to inform SUNAT about the identity of their ultimate beneficiaries. Nonetheless, up until recently, SUNAT was pending to issue a resolution establishing the procedure, deadlines and conditions in order to comply with such obligation.

In fact, on September 25th, 2019 SUNAT published Resolution No. 185-2019/SUNAT, which sets out all necessary elements for legal persons and/or legal arrangements to comply with said obligation.

As a result thereof, those who carry out businesses in Peru shall take into consideration the following:

1. Legal persons and legal arrangements required to identify their ultimate beneficiary

Legal persons domiciled in Peru and legal arrangements established therein (e.g. trusts, investment funds, consortiums, among others), are required to identify their ultimate beneficiary.

Such obligation also applies to non-resident legal persons that have incorporated a branch, agency or other permanent establishment in Peru; to legal arrangements established abroad whose manager and/or administrator is domiciled in Peru; and to consortiums constituted abroad that nonetheless have a Peruvian-resident party.

2. First group of legal persons required to submit the Ultimate Beneficiary Return

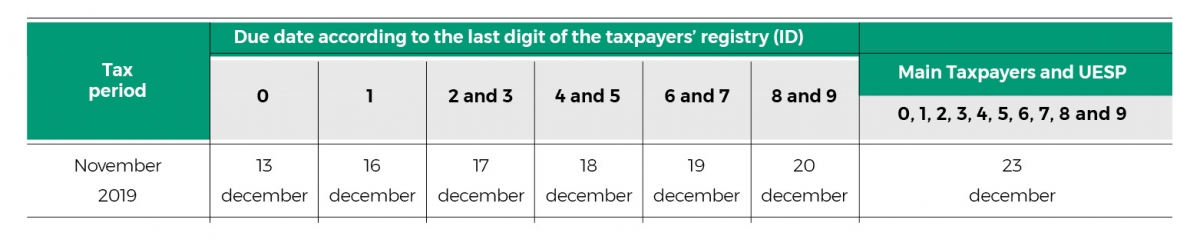

According to the Resolution, all legal persons that qualify as “Main Taxpayers” as of November 30th, 2019, are required to submit Virtual Form No. 3800 - “Ultimate Beneficiary Return”, in accordance with the schedule for monthly obligations provided by SUNAT for the period November 2019, as shown below:

In addition, the Resolution has established that the remaining legal persons and the legal arrangements must comply with such obligation on the deadlines determined by SUNAT in a future resolution.

3. Obligations concerning the identification of the ultimate beneficiary

Regardless of being a Main Taxpayer, all legal persons and/or legal arrangement shall take into account the following obligations:

- Submit “Virtual Form 3800 - Ultimate Beneficiary Return” through SUNAT’s Online Operations System, which will be available from December 1st, 2019.

Information related to the ultimate beneficiaries’ identity shall be attached to the Form by using an Excel application available at SUNAT’s Online Operations System. Nonetheless, said information may be entered directly into the Form, provided that only one (1) ultimate beneficiary is declared, who in addition to being a Peruvian resident, has a direct participation of at least 10% in the legal person.

Failure to submit such return may result in the imposition of a fine equivalent to 0.6% of the fiscal year’s net income (which will be no less than 5 Tax Units nor more than 50 Tax Units), as well as in the joint liability of legal representatives for any tax debt and in the inability to access certain notarial services.

- Obtain from the ultimate beneficiary the “Format of the Natural Person that Qualifies as the Ultimate Beneficiary”, available upon the entry into force of Supreme Decree No. 003-2019-EF.

- Keep the documentation and other information provided by the ultimate beneficiary evidencing its condition of such.

- Obtain proof of validating the documentation and other information provided by the ultimate beneficiary against the databases of RENIEC, SUNARP, SBS and SUNAT, among other sources of information.

- Obtain proof of the communication (or attempted communication) with the ultimate beneficiary or with the natural person of whom there is reasonable evidence about its condition of ultimate beneficiary.

- In case the ultimate beneficiary is unknown or if nobody meets the conditions to qualify as such, permanently publish such situation in their webpage’s home page; or, in case of not having a webpage, publish such situation once every fiscal year in the newspaper of largest circulation in the corresponding location.

- Keep updated information regarding the ultimate beneficiaries.

Any breach of these obligations may generate the application of fines equivalent to 0.6% of the fiscal year’s net income.

4. Updating information filed to SUNAT

In order to update the information consigned in the Ultimate Beneficiary Return and to perform any substitutions/rectifications thereto, taxpayers shall submit a new Ultimate Beneficiary Return within the deadlines established by the Regulation.

5. Substitution and/or rectification of the declarations

Moreover, the Ultimate Beneficiary Return may be substituted until the due date for its submission; after which, it may be rectified provided there is an error in the information consigned thereto.

6. Who is the ultimate beneficiary?

The ultimate beneficiary is:

- The natural person who directly or indirectly (i.e. through an ownership chain), has at least a 10% participation in the legal person.

- The natural person who directly or indirectly (i.e. through a control chain), has the effective control of a legal person.

- The natural person who occupies the highest administrative position in the legal person (i.e. CEO, board member or similar).

The criteria listed above shall be applied gradually (and not alternatively); meaning that, the second and third criteria shall only be applicable if the preceding criterion is not sufficient to identify the ultimate beneficiary.

For the specific case of legal arrangements, the ultimate beneficiaries are the trustor, trustee, beneficiary and any other natural person who, as a participant or investor, exercises effective control of the legal arrangement (i.e. influence on decision-making) or is duly entitled to obtain profits therefrom.

Contacts