NPLs: Second progress report by the European Commission and package of measures to accelerate the reduction of NPEs

Commentary 2-2018

On March 14, 2018 the European Commission presented the Second Progress Report on the reduction of non-performing loans (“NPLs”). The report comprises a memo and a factsheet, whose versions in English can be obtained on the website of the European Commission, which also distributed a press release (English version).

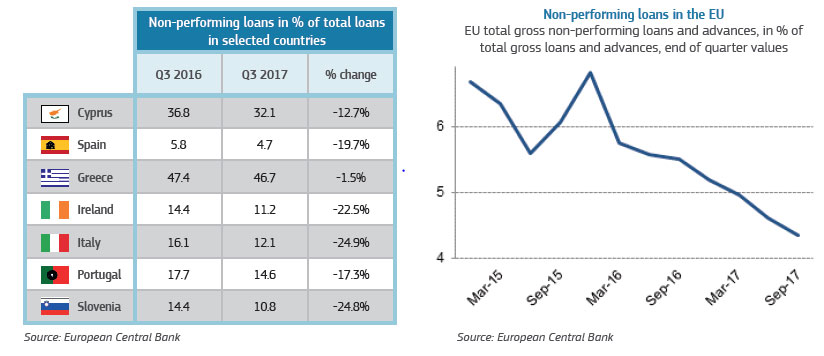

The Second Progress Report on NPLs confirms the downward trend of the NPL. In the third quarter of 2017, NPLs represented 4.4% of the total financing granted in Member States (as compared with 5.5% in the same period of 2016). In Spain, the decline in the percentage of NPLs was especially pronounced (19.7%), going from 5.8% in the third quarter of 2016 to 4.7% in the same period of 2017. Thus, in terms of percentage, Spain is placed at thresholds nearing the average of the European Union.

Nonetheless, the Second Progress Report also reflects the concern of the European Commission regarding not only the total volume of NPLs, which is still well above pre-crisis levels (€910 billion), but also the significant differences in NPL levels shown by Member States, which vary between 0.7% in Luxembourg and 46.7% in Greece. The European Commission also points out the slow decline in the figure of NPLs in certain countries, which it identifies as a major risk for the European Union as a whole.

For these reasons, and with a view to giving continuity to the Action Plan to Tackle Non-Performing Loans in Europe prepared by EcoFin in July 2017, the Commission calls for decisive progress to be made on the Banking Union. To do this, it adopts a “Package of Measures”, also dated March 14, 2018, for the reduction of NPEs (‘non-performing exposures’, which comprise NPLs in addition to dubious collateral and dubious assets off the balance sheet) which comprises:

1. Proposal for a Directive on credit servicers, credit purchasers and the recovery of collateral;

2. Proposal for the amendment of Regulation EU 575/2013 as regards minimum loss coverage for nonperforming exposures; and

3. Blueprint on the set-up of national asset management companies (AMCs).

The English versions describing and implementing these three measures can be consulted here.

The most significant aspects of the “Package of Measures” are described below:

1.- Proposal for a Directive on credit servicers, credit purchasers and the recovery of collateral

Credit servicers

- Creation of a common system of prior and mandatory authorization for servicers, which enables them to pursue their activity in the territory of a Member State, provided that certain requirements are met.

- Servicers previously authorized in a Member State will be able to operate throughout the European Union.

- Creation of a national register of authorized credit servicers in each Member State.

- Promoting loan servicing agreements (LSA) between financial institutions and credit servicers, for which mandatory requirements are stipulated.

- New safeguards and guarantees if the credit servicer outsources its work to a third party (credit service provider).

- Obligation for servicers to keep all correspondence with borrowers and all instructions received from creditors for ten (10) years and to make them available to the authorities of the Member State.

- New rules regarding supervision, administrative penalties and remedial measures directed at credit servicers.

Credit purchasers

Unnecessary impediments to the transfer of loans to third parties within the European Union will be removed through:

- The statutory recognition of a credit purchaser’s right to information.

- The use, by financial institutions transferring credits, of the technical standards provided by the European Banking Association (EBA).

- The prohibition imposed on Member States against imposing requirements other than those stipulated in the Directive on credit purchasers.

- The harmonization of the requirement for credit purchasers to inform the related Member State of transactions carried out in its territory, identifying the financial institution or servicer that is to be in charge of servicing the debt.

- The obligation imposed on credit purchasers without a registered office or establishment in the European Union to designate, in writing, a representative with a registered office or establishment in the EU, upon the conclusion of a transfer of credits.

- The obligation for credit purchasers or their representatives to report the terms of the credit purchased and to serve notice of their intention to enforce a loan directly or of subsequent transfers.

Accelerated extrajudicial collateral enforcement(‘AECE’)

- The objective is the swift out of court enforcement of collateral by way of public auction or private sale.

- The procedure is voluntary and must have been agreed previously with the debtor.

- The agreement represents a directly enforceable instrument and can be used, following notification of the debtor, within a certain period, which can vary between 4 weeks and 6 months after the event giving rise to the enforcement.

- The AECE will not apply to consumers and will be subject to the related insolvency regulations, should debtor be involved in insolvency proceedings, including the stay on enforcements pursuant to the insolvency legislation of the Member State.

- The AECE will require an assessment of the assets provided as collateral so as to ascertain the upset price of the auction or of the private sale.

- The debtor may go to court to challenge both the assessment of the assets and the use of the AECE, where the sale of the asset provided as collateral was not conducted in accordance with the national provisions transposing the Directive.

- The Directive provides that creditors must make reasonable efforts to avoid the use of the AECE.

2.- Proposal for the amendment of Regulation EU 575/2013 as regards minimum loss coverage for nonperforming exposures

Prudential backstops

The Proposal for the reform of Regulation EU 575/2013 as regards minimum loss coverage for nonperforming exposures, introduces the concept of prudential backstop for NPEs.

These are mandatory measures (in the form of minimum provisions or deductions from own funds) for newly originated loans.

Prudential backstops do not exclude the provisions that should continue to be adopted by the financial institutions of Member States pursuant to IFRS 9, applicable since January 1, 2018).

The text clarifies that the prudential backstop system will only affect NPEs originated after March 14, 2018, but not those originated previously. Nonetheless, those originated prior to said date and novated thereafter in such a way that the exposure of the financial institution is increased will be treated to all intents and purposes as newly originated and mandatorily subject to the new system.

3.- Blueprint on the set-up of national asset management companies or AMCs:

Interested Member States are given a non-binding blueprint on the set-up and development of AMCs at national level, in full compliance with EU banking and state aid rules.

The blueprint provides practical recommendations for the set-up, governance and action of AMCs, building on the past experience of asset management companies already existing in certain Member States, such as NAMA (Ireland, 2009), SAREB (Spain, 2012) and BAMC (Slovenia, 2013).

Contacts